At Melaleuca, we advocate getting out of debt! Debt makes everything you purchase a lot more expensive! And when you only pay the minimum payments, most of your money slips away as interest.

When You Have Debt, It Can Feel Impossible to Get Ahead

Consider a $10,000 credit card balance at 18% interest (roughly what the average US family owes in credit card debt). If you make a $200 minimum monthly payment, $150 goes straight to interest. Month after month, the lender pockets most of your effort while your balance barely moves.

The same trap awaits with homeownership—but the numbers are even more staggering. On a 30-year mortgage at today’s average rate of near 6.5%, you’ll pay more in interest than the entire value of your home. That $300,000 house? You’ll end up paying over $600,000 by the time it’s yours. And without a sizeable down payment, mortgage insurance only adds to that total.

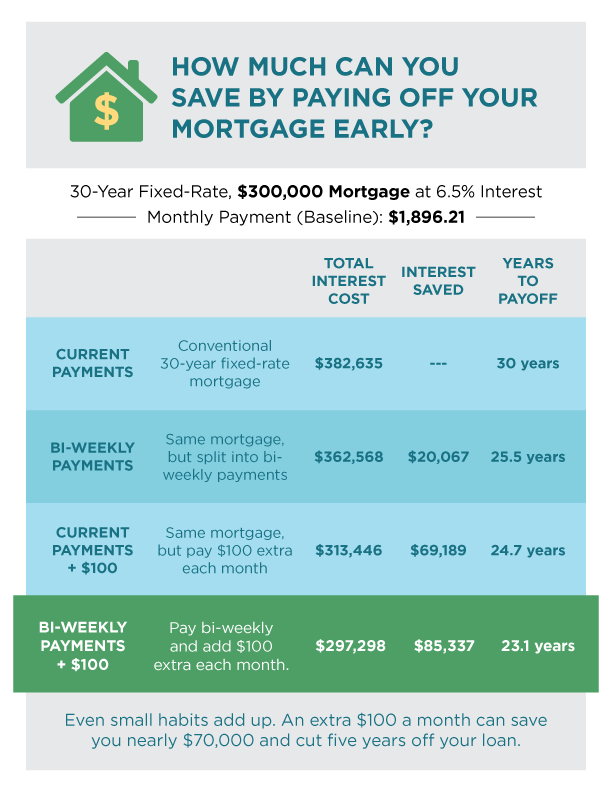

But a change in strategy can make a massive difference. On that same $300,000 mortgage at 6.5%, switching to a true biweekly (every two weeks) payment plan saves about $20,000 in interest and cuts roughly 4.5 years off your loan. Add just $100 extra each month, and you could save over $70,000 and finish nearly five years early.

Money and Health Down the Drain

Debt doesn’t just drain your wallet—it drains your health. Recent studies show that financial stress is strongly correlated with depression, and high household debt is linked to higher blood pressure. Overindebtedness can also lead to sleep disruption and greater use of sleep medications. In one study, people with debt difficulties were significantly more likely to have trouble falling asleep.

And if all that’s not bad enough, debt actively steals your future. When most of your paycheck is consumed by mortgages, car loans, student loans, and credit cards, there’s nothing left for savings, emergencies, dreams, or even to make ends meet. You’re working hard, but your money is already spoken for—claimed by lenders before you can use it to build a better life.

Simply put, debt is bondage, interest is the chain, and minimum payments are the lock. Together, they’re designed to keep you trapped. But the good news is that you can build a strategy to financial freedom— debt-free living. For example:

- Build a small emergency fund. Just $1,000 in savings can keep life’s surprises from pushing you deeper into debt.

- Cut the waste. Track every dollar. Slash nonessentials. Funnel the savings toward freedom.

- Increase your income. Put every extra check, bonus, or commission toward paying down debt—not lifestyle creep.

- Use the debt snowball method. Pay off your smallest debt first for a quick win, then roll that entire monthly payment into the next smallest debt. Early victories create momentum. That first paid-off card proves you can do it. The second falls faster. By the third, you’re unstoppable. Each eliminated payment becomes motivation for the next target—building both financial progress and psychological confidence.

- Pay off your mortgage early. Even small extra payments slash years and tens of thousands in interest.

Debt and interest can work together to steal your life, health, and peace of mind. But getting out of debt can win it all back. It takes focus and self-discipline, but it’s very much worth it!